Anuj Puri, Chairman – ANAROCK Property Consultants

Anuj Puri, Chairman – ANAROCK Property Consultants

2017 was quite an eventful year for the Indian economy at large, and the real estate sector got more than its usual share of the limelight.

A series of reforms and structural changes tore into the very heart of the industry, affecting a surgical strike at market opacity, unaccounted funds transactions and customer victimization.

The entire real estate fraternity had to re-orient their businesses to sustain in the changing environment.

Already, the real estate sector has shed a massive part of its unorganized and fragmented nature, and the ways and means of doing business in changed for good in 2017.

The incumbent Government maintained a laser focus on changing the fabric of the Indian economy, with direct implications on the real estate industry, by implementing highly impactful reforms:

- Cracking down on black money transactions with demonetization

- Setting up RERA – a regulator to increase financial discipline, improve transparency and empower property buyers

- Introducing GST to boost transparency in taxes and improve business efficiency

- Curbing anonymous property transactions and ownership by incisive amendments to the Benami Properties Act

Simultaneously, the Government’s ambitious ‘Housing for All by 2022’ mission also received a massive thrust in 2017 with the granting of the very vital infrastructure status to affordable housing.

In addition, the definition of affordable housing and houses classified under MIG underwent a series of tweaks to cover a larger buyer base and help developers offload their budget homes inventory.

Overall, 2017 saw the Government making it clear that home buyers will no longer be at the mercy of real estate developers, and putting various measures in place to ensure that housing supply syncs up with demand and pertinent projects are developed.

There are doubtlessly some teething troubles – some of them very obvious – in implementing and executing the new policies and reforms. However, they have made a deep impact even now.

Reputed global agencies have recognized the Government’s efforts in 2017 – India featured in the Top 100 nations in terms of ease of doing business as per the World Bank, and Moody’s elevated India’s sovereign rating from the lowest investment grade of Baa3 to Baa2, also upgrading its outlook from ‘stable’ to ‘positive’.

India Residential: Supply-Demand Dynamics

In 2017, new housing project launches were severely impacted by the triple tsunami of demonetization, RERA and GST. As per ANAROCK research, only 94,000 units were added in top 7 cities of India between Q1-Q3 2017, which is a drop of more than 50% from the same period in 2016.

However, the last quarter of 2017 looks encouraging – in the first two months of this quarter, around 18,000 units were launched, which is around 90% of the new launches in Q3 2017.

With restricted new launches and fence-sitters returning gradually to the market because of the comfort that the structural reforms and enhanced transparency provide them with), 160,000 units were sold during Q1-Q3 2017.

The decline in sales was only to the tune of 30% compared to Q1-Q3 2016. Unit sales have exceeded new launches for the consecutive six quarters, and the trend continues in Q4 2017 as well.

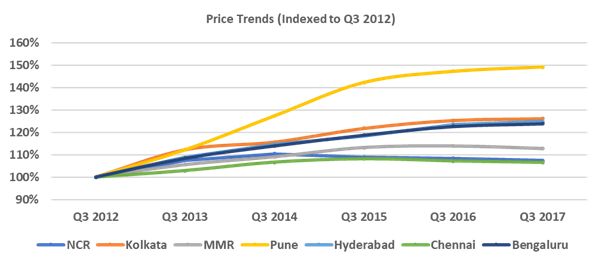

India Residential: Price Trends

2017 remained a buyer’s market throughout. The presence of a significant inventory of unsold units kept a tight control on average prices, which largely remained range bound between Q3 2016 and Q3 2017.

Assessment of average prices for the past 5 years (Q3 2012 to Q3 2017) reveals that Pune, Kolkata, Hyderabad and Bengaluru were the front-runners in capital value appreciation, bucking the trends of larger cities such as MMR and NCR.

India Residential: Unsold Units Trends

Unsold units in top 7 cities of India declined by 8% between Q3 2016 and Q3 2017. This decline was primarily due to restricted new launches amidst the green shoots of sales recovery.

The cities in South India recorded a higher decline in unsold inventory as compared to the other cities, primarily due to strict control on new launches and the dominance of end-users in these cities.

Unsold inventory decreased by 22%, 18%, and 16% in Hyderabad, Chennai and Bengaluru respectively between Q3 2016 and Q3 2017. NCR and MMR, which account for around 55% of total unsold units across top 7 cities as of Q3 2017, witnessed a mere 6% decline in unsold units between Q3 2016 and Q3 2017.

In the post-RERA era, developers are focusing firmly on executing under-construction projects within the stipulated timelines; new launches are likely to be restricted, and unsold units will decline further in 2018.

India Residential: Unit Size Trends

With changing buyer preferences and skyrocketing prices, developers have been compelled to construct compact homes.

As per ANAROCK research, the average size of new units launched in 2017 has shrunk significantly over the previous year, across the top 7 cities of India.

Notably, NCR witnessed the highest reduction of 21%, followed by 15% reduction in Pune, Kolkata and Hyderabad, and 12% in MMR.

Wrapping Up

Real estate developers are unlikely to forget 2017, which was like a bad dream come true, and look forward to better business in 2018. For sure, home buyer confidence is reviving, and more fence-sitters will spring into action in 2018.

- Overall, 2018 will be a year of market recovery defined by restricted new launches, gradually improving sales and declining unsold units

- With a massive focus now on affordable housing, this segment will be the poster boy of 2018

- A notable phenomenon in 2018 will be a large-scale consolidation of developers and brokers, and distressed assets changing hands.

We may not see a scintillating residential market recovery in 2018, but it is certain that whatever recovery and growth we see from here onward will be sustainable and backed by stronger market fundamentals than ever before. The days of speculative peaks and troughs are safely behind us.